Below is a copy of the minutes of a meeting I had with BAP and the various custodians. I chose to copy and paste the document from the original Adobe PDF format rather than post each page as a picture for clarity and ease of reading. I will post the attachments mentioned in the document in a subsequent post.

MEMBERSHIP MEETING WITH TREASURER NORMAL L. LASALA February 8, 2005, 4:00 PM, BAP Office 11/F, Sagittarius Bldg., H.V. Dela Costa St. Salcedo Village, Makati City Attendance: DoF Usec. Eric Recto

BTr Treas. Norma Lasala

Dep. Treas. Ed Mendiola

Atty. Elna Cruz

Dir. Nanette Diaz

Ms. Edna Bona

BAP Pres. Cesar E.A. Virata

Treasurers of Member Banks

Custodians Citigroup

PDTC

IntroductionSee pages 10-14 Introductory Speech delivered by Treasurer Norma L. Lasala

Open ForumAtty. Cruz: The DoJ Opinion mentioned the so-called “conflict of interest” of the BTr

to be custodian and registrar at the same time. BTr wanted to exercise supervisory functions over the banks which are under the supervisory function of the BSP.

The BTr needs to clarify these things because the Bureau do not want to exercise supervisory functions over the banks but since the BTr is in-charge of RoSS, its sensitivity and mandate, the Bureau needs to ask certain questions so that the BTr can perform the appropriate due diligence. For the BTr not to even as ask questions and just accept everything without even

looking into these things will mean that the Bureau did not exercise the due diligence which will be tantamount to negligence.

The BTr hopes that these will be understood by the banks that such do not mean that the BTr want to exercise other agency’s functions. But there are certain things incumbent upon the BTr because of the mandate and the sovereign issue involved. There are other issues being looked upon for clarification which the BTr feels need to be resolved before moving any further which cannot be accomplished overnight.

Treas. Lasala: Currently, the BTr is trying to enhance the capabilities of RoSS so that the

Bureau will be in compliance with international accounting and auditing standards and all other global standards with respect to government securities. What is essential is to be able to segregate of the account held proprietary which can be done in the RoSS so that the repurchases held by the banks can be disclosed and can disclose it properly. The BTr does not want banks to be in violation of rules and regulations regarding repurchases.

Dep. Treas. Mendiola: Switch-auction. Objective: To be able to reduce the number of outstanding issues in the market. The BTr will announce what particular securities the Bureau would like to buy and the bank will then submit to the BTr competitive offers to sell that particular GS. The BTr will try to buyback all the illiquid GS and achieve the reduction of the number of ISINs.

The BTr believes that by doing so, it will improve the liquidity in the market. The announcement of which bonds will be the subject of the switch- auction will be made using the wires available to all banks. The pricing will be done on a multiple price basis obtained in a Dutch Auction method. Only eligible dealers will be eligible to submit offers with minimum offers of PHP10 million.

(The detailed procedures of the Switch-Auction will be provided to the banks the Dep.

Treas. for comments)

Treas. Lasala: The BTr will announce the prices with respect to dealt transactions (as

against with the MRTN or with respect to the yield that is fixed on a daily basis. The banks may want to review this pricing method and contrast with the current valuation method. If it is useful, it can be used to value the both proprietary and the clients’ holdings of the banks which are with the BTr. This shall be made available via SMS.

Dep. Treas. Mendiola: The BTR can determining the average done deals since they are captured in RoSS. The BTr is currently finalizing the MTM formula of valuation. This will be announced through the wires and via SMS which include the auction and the real time done rates. Comparing with Bloomberg rates was not far from the rates captured in RoSS.

PBCom: The banks would like the status and reaction of the BTr on the issue of the BTr acting as registry and as a custodian at the same time is not acceptable as mentioned in the DoJ opinion.

Atty. Cruz: The BTr is seeking clarification on several issues with the DoF. The details, however, cannot be divulged as of the moment so as not to preempt and out of respect to the DoJ. As of now, there is no final, final opinion/resolution on the matter.

USec. Recto: If (I) understood the circular correctly, the BSP is not objecting to the RoSS acting as a third party custodian. It’s not a mutually exclusive situation that the circular envisions. The BSP is not objecting to the BTr acting as a custodian as well. But what the BSP wants is to grant an option to the investor to choose another party to act as custodian. (I) hope this is clear

with all of you here. If not, then (I am) telling you that that is (my) interpretation. AG Nesting Espenilla has not opposed that interpretation. Is it your understanding that Circular 392 or 428 prohibits the BTr to act as a third party custodian? If this is the case, (I) do not agree with that interpretation because (as I have said) the circular just wanted to give thepublic the option to choose a custodian other than the BTr. The BTr is not forced to move out all securities purchased if the investors decided not to.

PDTC: Clarification on USec’s statement: The circular says that the RoSS can act as a registry but not as third party custodian. Actually, the investor has two alternatives: (1) name on registry with the RoSS as registry; and (2) go to a third party custodian.

USec. Recto: What is the default choice if the investor do not want to put the securities to

a third party custodian?

PDTC: The default choice is always the RoSS as a registry.

USec. Recto: Therefore, the RoSS acts as a de facto “custodian” if the investor does not want to put his/her security to a third party custodian and just maintain it in the RoSS. (My) reading of the circular is for the investor to be given a choice where to put their securities. What then will be the first choice of the investor is he does not want to bring it to a third party?

PDTC: The first choice of the investor is really to go to the RoSS but it is actually a name on registry and the RoSS then is acting as a registrar but not a custodian.

USec. Recto: So if the investor (as I said) does not want a custodian? What will be the

situation when (I) Eric Recto purchased a GS and (I) do not want to put it to a bank not because (I) don’t like them but because it is more convenient (for me) to keep it with the BTr for one reason or the other? Is your understanding with Circular 392 that (I) the investor is prohibited from keeping the GS at the BTr?

PDTC: No, that is your first choice actually.

USec. Recto: Then, if that is the case, what role does the Treasury play at that point? It is

in fact a custodian as well, de facto.

PDTC: (BTr) as a registry, only because there is a differentiation between the registry

and the custodians in terms of (value-added) services.

USec. Recto: Ok, in terms of services. (I) think we might be mincing words here. What (I) want to point out since there is a fine line that everyone should understand. The BSP is not compelling the investors to place the securities that he invested in to another party other than the RoSS/BTr - the BSP is not! So that the investor has the choice to keep it in the Treasury and (as I said) de facto Treasury acts as a custodian in a more generic definition of the word custodian. On the other hand, the definition of a third party custodian as opposed to the former, (I) agree is different. These differing services are the impetus for the investor to appoint a third party custodian. Agree that (a) the BTr cannot act as a third party custodian because it is not a third party because it is the issuer; (b) that the BSP is not compelling the investor to lodge the securities to an entity other than the BTR; and (c) The definition of a custodian as providers of services and the BTr in a de facto situation where the investors do not want to move their securities are two totally different things.

Citigroup: When the investor does not want to move his/her securities and maintain it to its current position in the RoSS it is referred to as self-safekeeping.

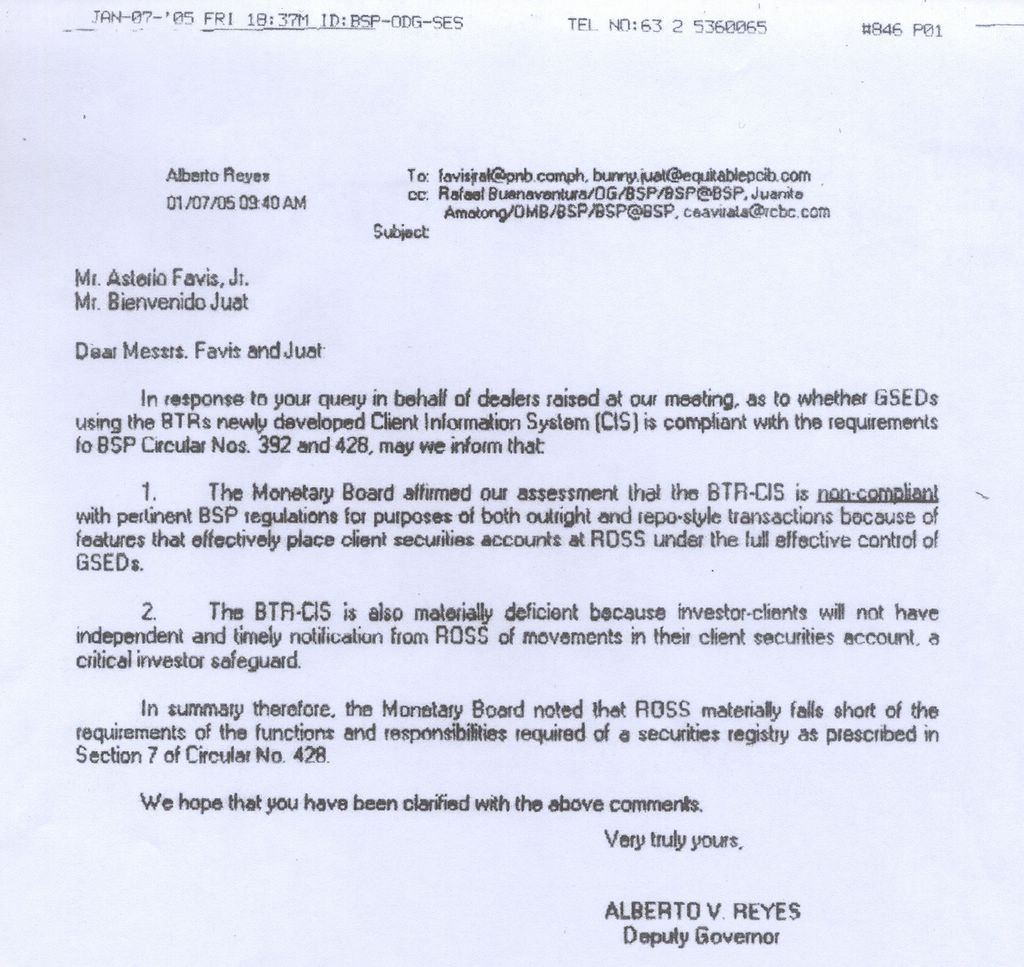

Metrobank: From the banks initial reading of Circulars 428 and 392, the bank understood

that registry by name as specified in the circular is compliant with Circular 392. The circular is silent whether the registry by name will be with the BTr or with any other party. So the banks were hoping and made to believe or the banks understood it that registry of the client’s name with the BTr is compliant with 392. This was the understanding of the banks until the banks

received a letter from Dep. Gov. Reyes (See page 15) saying otherwise i.e. registry by name with the BTr is not compliant with Circular 392. That is where the banks stand right now and do not know where to go from there.

Treas. Lasala: (We) have been in the market for a very long time and Pres. Virata have been

here far longer and he knows that any BSP Circular or any MB Resolution cannot be amended by an ordinary letter. It can only by amended or superseded by another Circular.

Metrobank: That was a very good clarification. However, (Mr. Virata) can (we) seek

clarification to the BSP on this particular letter by Dep. Gov. Reyes.

Pres. Virata: There is one clarification with DoJ (by BTr) and a clarification to the BSP (by

BAP) where the clarification with BSP may run in conflict with the BSP Circular or DoJ’s opinion on the clarification made by the BTr. This is a series of clarifications. The BTr will reduce the number of securities which the banks appreciate.

ING Bank: January 31, 2005 was the deadline given to the banks to do a reclassification

of securities that should be under HTM, ASS and TAS. Does the BTr taken this in consideration since this will impact the banks booking of securities considering the requirement of IAS 39?

Treas. Lasala: The BTr is looking to announce it way before hand so that the banks can

look into the ISINs and determine who are holding these securities in the banks’ accounts. There are also other strategies that can be employ so as to address accounting issues with respect to the classification of securities as to HTM, ASS and TAS.

Membership Meeting with Treasurer Norma L. Lasala

Page 5 of 9

Pres. Virata: Issues under IAS 39, the moment the banks move a portion of the IBODI

will already be considered tainting. (I) hope this also addressed.

Metrobank: May (I) suggest to include the accounting professionals in addressing the IAS

39 issues in the possible movement of securities or new strategies and plans related to this matter since they will be determining whether there is tainting or not and will be qualifying the banks’ accounts and invoke the international accounting standards.

Pres. Virata: The Treasury should consider that because the portfolio of the banks will be

greatly affected.

Treas. Lasala: (Nods.)

EQPCIB: Regarding the DoJ clarification, did they give any time frame when are they come up with their clarification?

Atty. Cruz: Unfortunately not, they did not give a specific time frame.

Treas. Lasala/USec. Recto: (DoF/BTr) will follow up.

EQPCIB: While (we) are waiting for the DoJ clarification, going back on the issue on name on registry, was there any discussion with the BSP, if the implementing procedures is in compliant with what is the spirit of the Circular because there are two approaches (1) name on registry and (2) appointing a third party custodian bank?

Treas. Lasala: BTr is proceeding according to the mandate and to the objectives that is shared by the BSP in its circular (policy statement) – “To promote the protection of investors in order to gain their confidence and encourage their participation in the development of the domestic capital market. Therefore the following rules and regulations are promulgated to enhance the

transparency of securities transactions with the end in view of protecting investors.” The BTr embraces the same objective and moving along the same objective.

Metrobank: Moving on to documented repo transactions. The circular is specific to delivery to a third party custodian for a bank to enjoy the 2% reserve requirements, the banks also want to implement this to start the documented repo transactions (or on-books repo transactions). On this note, may the banks be updated whether the third party custodians that have been accredited will be linking with the RoSS to be able to allow the banks to do documented repo transactions.

Treas. Lasala: There are two groups right now: (1) banks who are accredited custodians are

already linked with BTr via Moneyline Telerate and they have a separate proposal for that; and (2) non-bank also has another set of proposal. The BTr has yet to see a harmonization of proposals.

Pres. Virata: Apoy (Mr. Go of Metrobank), does that impede your trading? (Addressed to accredited custodians) Will the connection to Moneyline Telerate will already enable them to start relationships with banks who would like to appoint them as third party custodian?

Citigroup: As far as the systems of the global custodians are concerned, (our) systems

ready if Dep. Treas. Mendiola agrees.

Dep. Treas. Mendiola: Discussions and negotiations have already been made but the registry

will be compromised if the BTr will open it as a nominee or a trust arrangement. As far as connection is concerned, they are already linked via the Moneyline Telerate but as to the use of the account, the BTr is still getting a legal clarification on the matter since the Registry has been defined, in so far the existing regulation are concerned even issuances of the DoF, has always been defined as registry of ownership. This is the reason why the BTr cannot open a nominee account unless they have a strong legal opinion on this. Hence, BTr offered an alternative which the accredited custodians can easily operate even today that is to connect the custodians wherein the custodians submit to the BTr the necessary requirements. The BTr can discuss this arrangement in another session related to the Working Group chaired by USec. Recto. The BTr is already working on opening an account whether it is a nominee account or holding account. The (GS) holdings of the clients of the banks that will be delivered to a third party should definitely has to be registered with the RoSS.

Metrobank: (Addressed to Pres. Virata) Right now, the banks cannot trade documented

repo yet.

USec. Recto: (We) The Working Group (composed of DoF, BTR, BSP and the accredited

custodians) are meeting weekly to find a solution. In a matter of week or so, this issue should be resolved.

(Mr. Go thanks USec. Recto)

Pres. Virata: Is the average price for the day good enough for MTM?

ING Bank: Will the average price be obtained from interbank only?

Pres. Virata: If only interbank, therefore it is not a full market?

Treas. Lasala: This (average price) does not include trades done among the banks’ clients

only among interbank transactions. If the BTr adopts this, will this be a fair

pricing?

Membership Meeting with Treasurer Norma L. Lasala

Page 7 of 9

HSBC: There are different parameters used when computing the price, did the BTr

looked into this?

Treas. Lasala: Yes, the BTr looked into these before the RoSS and did a lot of exercise to

arrive at the number and compared it with what the banks are getting in the (sophisticated) MRTN.

Pres. Virata: Is this good for all investors in GS if it is purely determined by transactions

among financial institutions? Is it going to be a good market?

HSBC: Currently, that is how the market is being priced i.e to get the 60% of the best bid among financial institutions to arrive at a benchmark.

Pres. Virata: According to the Treasurer, the BTr has the facility to compute of the average price on done deals.

Metrobank: And interpolated for those tenors where no deals have been done. (Treas. Lasala nods.) Sounds reasonable.

Chinatrust: What will be the procedure if there are no (almost zero) deal trades happening in the market (e.g. July to November 2004)? If the market will use previous day averages for what is today, it will be quite ticklish. If it continues to moves on (I) don’t think it is a good MTM procedure to adopt as well.

Treas. Lasala: In the absence of a dealt transaction, (I think) it stands to reason to adopt what is there – the only reference price available. What is a better alternative? (I think) there is no better alternative in the absence of any done transaction.

HSBC: (To clarify the Treasurer’s reply) The Treasurer would like to refer to the previous day’s (sophisticated) MRTN’s closing price if there are no done deals. (Treas. nods) Otherwise, the only alternative will be the bids from which the market is currently using.

Chinatrust: (I think) this will be quite dangerous especially if it comes to a prolonged market of no done transactions. Can the system go back and revert to getting bids (otherwise called as the MART01 format)? Again, (I guess) it needs to get into consideration the use of Bloomberg. Another question, how will the BTr define on-the-run securities – will it be inconsonance with

the same definition that the MART has implemented because the MART has already expanded its definition of on-the-run issues.

Treas. Lasala: This should not be a problem. The BTr will define the same tenor buckets

of liquid benchmarks very similar to currently market convention defined by MART.

Membership Meeting with Treasurer Norma L. Lasala

Page 8 of 9

(Mr. Avante thanks the Treasurer)

Pres. Virata: How about the banks’ currently market practice on trading based on yield of

specific tenor buckets and no on a per security basis? Will this be captured in any of these systems?

HSBC: Addressed to Pres. Virata: (I think) you are referring to how many are the benchmarks? The answer – there are roughly 15 benchmarks that the banks priced. The benchmarks are priced and correspondingly the prices are in between or interpolated MTM price. If the question arise from the point of view that there are roughly 356 securities lines, then the banks’ reply will be – there are no existing facilities to price these 356 bonds but price the 15 and interpolate the ones in the middle.

Treas. Lasala: That is what the BTr hopes to remove the so many intervening ISINs soon.

Pres. Virata: How much is the amount of borrowing of the government programmed for

2005?

Treas. Lasala: NG will borrowing PHP600 billion for the year 2005. Forty percent (40%)

of which are foreign borrowings while 60% are domestic (included NPC etc.). This is the biggest refinancing so far, hence it is critical that the BTr does it correctly and will not have too many peripheral issues unsettling the market. The BTr wants to focus on actively managing it this time so that having done so, the market will have a window of opportunity to effect real reforms in all sectors. The NG is looking to incur a budget deficit as planned of PHP177 billion (cash deficits only) which include the PHP18.8 billion in interest payments from NPC. The consolidated public sector deficit covers government and GOCCs plus other government financial institutions excluding BSP and the pension funds.

Metrobank: Does the PHP600 billion planned borrowing already taken into consideration

the impact of the tax measures being approved right now? If so, how much is estimated to be part of the PHP600 billion.

USec. Recto. For purposes of planning, (we) have only considered tax measures that have

been passed such as the sin tax law, the effect of the lateral attrition among others.

Pres. Virata: Are all the issues with withholding taxes or some of them taxable?

Treas. Lasala: Unfortunately, the BTr cannot accommodate the NOLCOs that are being

booked by the bank since there will be no forthcoming issues that will be taxable.

Pres. Virata: Right now, the BIR has also changed a number of their stance i.e. whenever you invest in a GS, it becomes a deposit substitute therefore taxed at 20% withholding which (I think) is not a correct definition of what a deposit substitute should be.

Treas. Lasala: The BTr is meeting with the BIR every so often and (we) will take this up if

you wish.

Metrobank: (We) can try to make this forum more often.

ClosingPres. Virata: (I suppose) after the clarification, we can move forward and hopefully

transactions especially for the forthcoming issues for the FY 2005 amounting

to PHP600 billion, there will be more trade.

Thanks the Under Secretary, Treasurer and Deputy Treasurer to joining in

the BAP Treasurers in the forum.

(Applause)

Treas. Lasala: Thanks Pres. Virata for granting (her) request and joining in the forum and

the Treasurers of the BAP member banks. The BTr to be of assistance by

way of informing the banks of recent developments or programs the Bureau

are crafting for the broadening of the capital markets.

End of Discussion