Getting things done RIGHT

Proposed Schematic I was working on last year with the BSP

b) Secured the necessary budget to effect the following enhancements for RoSS;

c) Announced a 31st March 2005 initial delivery date to the GSeD community through Bloomberg to begin meeting the requirements of the GSeDs and custodians;

From November last year to the time that I left, we could not seem to make headway with respect to our proposal.

With this as historical context and reference, it is critical to understand the significance of the re-articulated position paper of the BSP as released by them through the BusinessWorld edition of 11 March 2005.

In the Arguments Section, the BSP said,

"...What this means is that, in the case of government securities, the investor may take direct delivery of securities bought by instructing the dealer to instruct RoSS to credit his securities account. This is perfectly acceptable, provided that RoSS has the capability to directly confirm to the investor his transaction on a timely basis.

However, the Client Interface System of the RoSS is deemed non-compliant at the moment because of this material deficiency, as well as its inability to render periodic securities statements directly to the investor. It will be considered compliant as soon as these deficiencies are remedied."

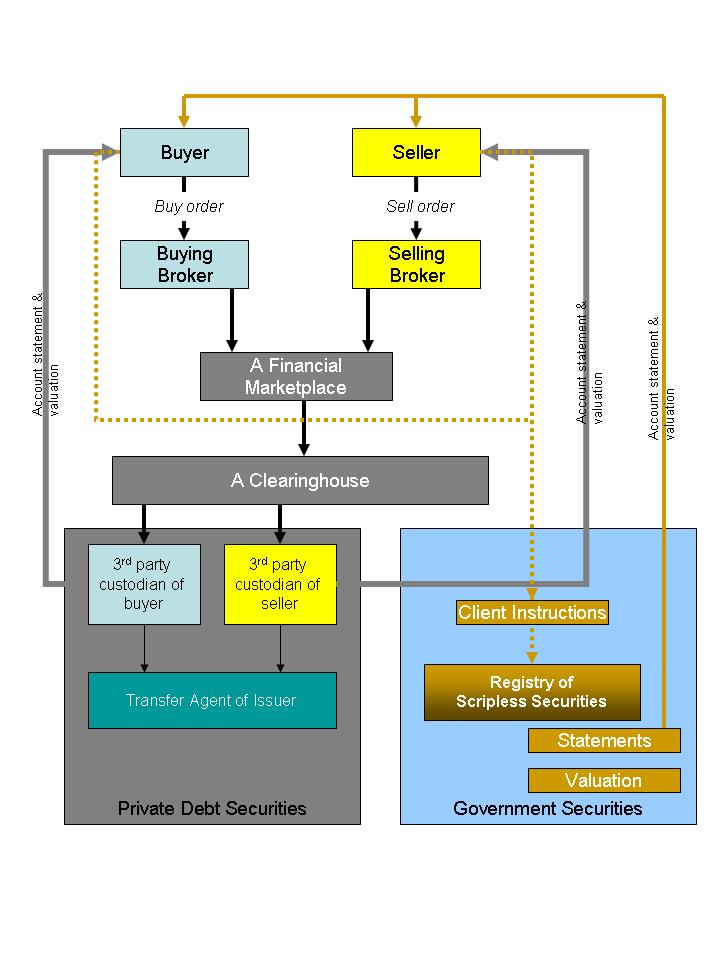

Rather than resort to 3rd party custodians for safeguarding the investor, the investor protection mechanism that the BSP is affirming is that provided there is an independent means for the investor to be informed of what is going on with his securities account, then the BSP is meeting part of its objectives. At the same time, by empowering the investor direct access to RoSS, we would be joining a select group of countries in terms of best practices for investor protection. The readers might want to refer to the Direct Registration System implemented in the US by the Depositary Trust Corp. last year following a 1994 exposure draft issued by the US SEC. (please click on the links to the referenced sites)

In addition, with the BSP agreeing to BTr pursuing our original proposal, we would also be able to resolve the ticklish issue of costs for implementing 392. Because the BTr already has an approved budget, we would then be only talking about a very small one time cost. Any way you look at it, I would like to think it is WIN-WIN for all the stakeholders.

As an aside, the BSP and readers may be interested to know that even before I left, the BTr was already doing test SMS messages for government securities (GS) informing investors of the latest GS prices through their cell phones.

For the very specific issue of investor protection, I leave it to BSP, BTr, and the GSeDs to earnestly study the abovementioned recommendation which is realistic, proven, and deliverable.

I believe the foregoing to be in the realm of operational issues and approaches.

What will continue to be troubling with respect to Circulars 392 and 428 deal with the legal aspects surrounding such issues as:

1. GS issuances and RoSS are strategic infrastructure that the government relies on for its funding requirements. Again, what is the proper disposition of government infrastructure? What is the proper means for accessing government infrastructure?

2. To use Sen. Roxas words, can regulatory fiat be used as a substitute for legislation in creating franchises? Does it make sense for the national government to limit the trading of its securities to a single market? Would building capital market infrastructure need to be bid out ala Italian Treasury and everywhere else there is an exchange centralizing GS and seek enabling legislation? (This is a point that the people in FIE seem to gloss over whenever they cite these examples of "G-30 best practices");

3. Where are the regulatory boundaries between SEC and BSP? We are talking about efficiencies and transparencies related to securities and yet the BSP is setting the agenda? How do we avoid overlaps and opaque and conflicting operations in the future;

4. Should an exchange be deemed as a quasi-public entity, more in keeping with a franchise? If so, should its revenues be subjected to a cost-recovery formula that is approved by a toll-regulatory commission no different form other utilites. Should major expense items such as IT infrastructure be supervised because the amortization costs of these decisions are still passed back to the investor and government alike?

5. How should we understand the term "disadvantageous the government". Shouldn't all the purported benefits and overall reductions in costs be quantified and guaranteed by the proponent similar to the way other privatized utility operators have been required to do.

posted by Nina at 11:40 PM

![]()

![]()

13 Comments:

In the last four weeks that I have been following this Blog, I must admit my disappointment and embarrassment at how my profession has torn itself apart.

On one hand, the very public disagreements plus the juvenile insults make me cringe that this is available for global viewing.

On the other hand, Mrs. Lasala is making me think the unthinkable - that we did not do our homework, and that we are peddling something which is obsolete as best practice.

As a trader to other fellow traders, I think we all need to reconsider our positions and begin to think about cutting our losses.

Remember the old adage, bulls make money, bears make money, but pigs always get slaughtered.

3:54 PM

One major issue that must be adressed is that imposing a third-party regulation on governemtn securiteis trading may, in addition to the costs of custody, add risk premiums to investing in government securities.

Regardless of how strongly a private firm is capitalized by its invetors, that firm cannot hope to even come close to the rating of a sovereign.

The RoSS is wholly owned by the Republic of the Philippines and all risks from direct on-registry are sovereign (i.e. negligible).

A non-sovereign custodian has the added dimension of custodial risk (the risk the custodian will screw up) not to mention the operational risk of the added layer of operations.

The concept of direct on registry ownership may have additional benefits as well for the government. It will permit the governemnt to tie investment income to a specific holder for purposes of taxation making with holding of taxes on interest at source unnecessary for purposes of collection (although it will continue to be important for purposes of the government's cash flow).

The objectives should not be to get rid of the Financial Reforms Project but to make the financial reforms project work for all parties concerned so that in the long run the entire market and not just a section of it benefits.

8:30 AM

The Joker is touching on a significant set of policy issues that the Philippines would do well to consider.

He/She raises an interesting point that having a custodian outside of RoSS for GS would mean that we in the market are taking on custodian risk. In effect, what I think the Joker is saying is that the government (BSP and DoF) are actually promulgating a policy of debasing a risk free standard and replacing it with an inferior product for investors.

One could argue that this is no different from debasing coinage or legal tender. By introducing volatility and risk in an area where there is none today, the BSP Circulars could be said to be inadvertently injecting inflationary pressures into the economy. How then does this reconcile with the fact that the BSP's mandate is sound monetary policy and inflation management?

The second point raised is that Direct Registration actually will lead to deeper liquidity. Since government need not guess the applicable tax rate for the investor, as he already knows who the beneficial owner is, the artificial segmentation of taxable vs. tax withheld GS can be removed. This creates a homogenous market. If the BSP is pursuing price discovery as one of its market reforms, then a more liquid market, presumably, will give better pricing.

4:01 PM

The article is very simple and clear. The question that needs to be asked is, "Is it fair to the Phil. Government and the Filipinos to merely GIVE ON A SILVER PLATTER (as in really GIVE without any compensation OR ANYTHING) a government infrastructure (RoSS) to a private group and select banks where (1) the government has invested a lot of money and the said private group and the selected banks stand to earn billions of pesos EVERY YEAR; and, (2) twiddle with a system (RoSS) that has been determined to be proven, reliable and secure AND ACCEPTED!

Maybe the bright boys in BSP can train their attention to safeguarding investors like looking at transactions of Standard Chartered Bank (who, by the way, is one of those banks "ACCREDITED" by BSP as a third party custodisn) and other similar banks who may have done similar offerings?

BSP boys, Omar Cruz, please look into you conscience and see if what you are pushing to implement is realy for the GOOD OF THE FILIPINOS.

10:45 AM

I read in the papers today that the FIE pushed through with its launch today. Am curious to know how they did the trading and how these trades were cleared and settled...unless BTr does a 360 and allows PDTC to connect, how will settlement and securities delivery be done? Does anybody have any info?

4:44 PM

Today's launch only involved the trading system of the PDEx and at that it involved a semi-parallel run. Clearing and settlement continues to be via individual trade processing using the RoSS-PhilPASS DVP link for financial institutions.

5:28 PM

"semi-parallel" run. What does this mean? Are the transactions consummated through the system binding on the part of the transacting parties? If only the front-end is being tested... Is the above poster therefore saying that it is business as usual in terms of how the trades are confirmed, how COS/COP transactions are initiated, and how these transactions are relayed to the custodians and in turn relayed to RoSS?

In other words, are you saying that only the telephone method of trading was replaced yesterday???!

10:17 AM

In a word, yes... and the above poster is just as puzzled as you are how this is supposed to be "best parctice"...

10:20 AM

If this FIE thing is already an obsolete best practice as mentioned and will not add any value to the whole system, then why are these bright boys cannot simply admit their mistake and go study other options and choose the best for all stakeholders.

Or maybe the millions is just too enchanting and magical that they just doesn't care if its evil or not.

The sad part is that they will be enjoying their millions at the expense of the investors and the government that need every centavo it can save to survive.

I wonder why Malacañang is very quiet about this issue. Is there somebody up there who will benefit from this FIE? Just asking!!

11:15 AM

System was down this morning for Metro, Stanchart, BOC, Chinatrust, etc.

Growing pains, I guess, are to be expected. My question is, BAP agreed that all traders are prohibited from using the phone, if the market is moving, how do I protect my bank and my investor if I cannot get my ####!!!! trades into the system?

Another question, what if I do the trade by phone and post my COS/COP through Telerate? (just like I have always done)

a) who will know?

b) am I cheating?

c) but I protected myself against a fast moving market

If the FIE cannot guarantee 100% uptime, which no system can really deliver, am I not duty bound to disintermediate the exchange?

This is different from the NYSE when 9/11 happened. In that case, since the systems are so interconnected, there was no trading to speak of. Nobody was at an advantage or disadvantage, unlike the banks who were offline this morning. Such is not the case with the FIE and GS since the various legs are disconnected and old means of transacting are still in place (you can't kill off the old systems either because that is "best practice" for business continuity).

5:34 PM

The Chicago Board of Trade, where Futures are traded, is a true exchange. Each participant has as their counterparty risk, the exchange itself and not another entity. Of course, the CBOT is hugely capitalized. The FIE is not. So, the FIE is just another pretender exchange.

Also, I heard that the onerous contract for the FIE states that the FIE does not have any liability after the contract of the FIE with the service or system provider expires. With this type of contract, how can anyone have faith in the FIE?

And the BAP would have all banks swallow this contract. Wow, talk about taking leave of one's senses......

1:27 PM

the World Wide Web is home to a great number of marketing opportunities that you could avail of,

3:56 AM

hollister co

fitflop uk

ghd hair straighteners

ralph lauren uk

longchamp pas cher

basketball shoes

ugg outlet

nike free runs

nike sb

tommy hilfiger outlet

cheap uggs

instyler max

polo ralph lauren

timberland uk

vans shoes

gucci borse

nike trainers

hermes belt

ray-ban sunglasses

sac longchamp

canada goose outlet

nike cortez

snapbacks wholesale

sac longchamp pliage

cheap uggs boots

oakley sunglasses wholesale

mcm outlet

nike air max 90

mont blanc pens

tod's shoes

2:05 PM

Post a Comment

<< Home