RoSS as a golden parachute

By SEN. AQUILINO PIMENTEL

Privileged speech delivered on March 14, 2005

Recently, the mass media reported the ouster of the National Treasurer, Ms. Norma L. Lasala, barely four months after she assumed the office. It was the shortest term served by a treasurer. It was so efficiently executed that long before the appointment papers of her successor were signed, the major dailies already announced her replacement with certainty.

Why? What triggered her unceremonious removal from office?

Outright Injustice

It certainly wasn’t because she had done something wrong as her superior, Secretary Cesar Purisima, had so unfairly insinuated in the press that the Department of Finance “had something against her.” Because if that were so, fairness dictates that the department should reveal what wrong she had done. But to simply imply that she had done something wrong without backing it up with proof is to my mind not only malicious but an outright injustice to the national treasurer who was merely trying to do her duty as best she could.

What, then, has she done to merit her removal?

Denouncing BS Circulars

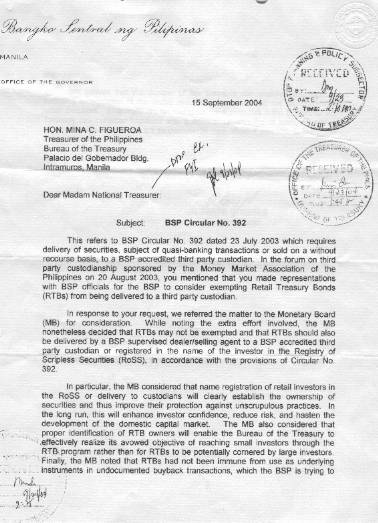

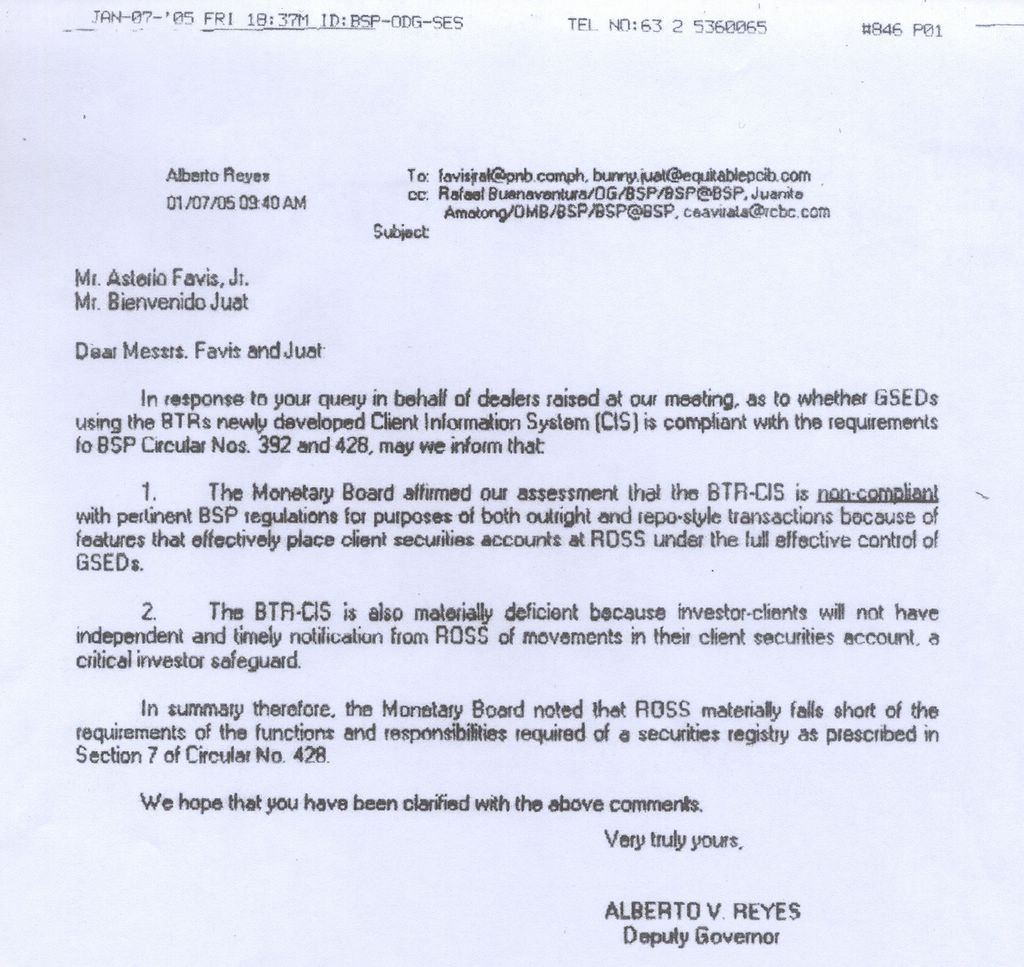

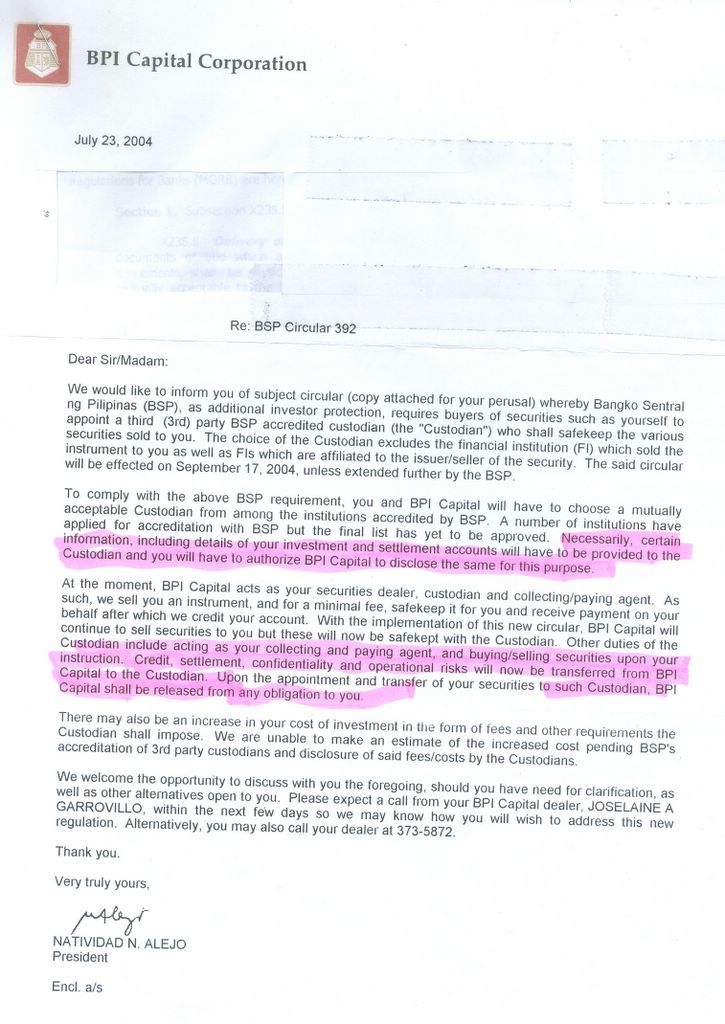

The thing that apparently triggered her dismissal from office was her having categorically objected to the issuance and implementation of Bangko Sentral Circular Nos. 392 and 428 which created the so-called Third Party Custodians in the securities market of the country.

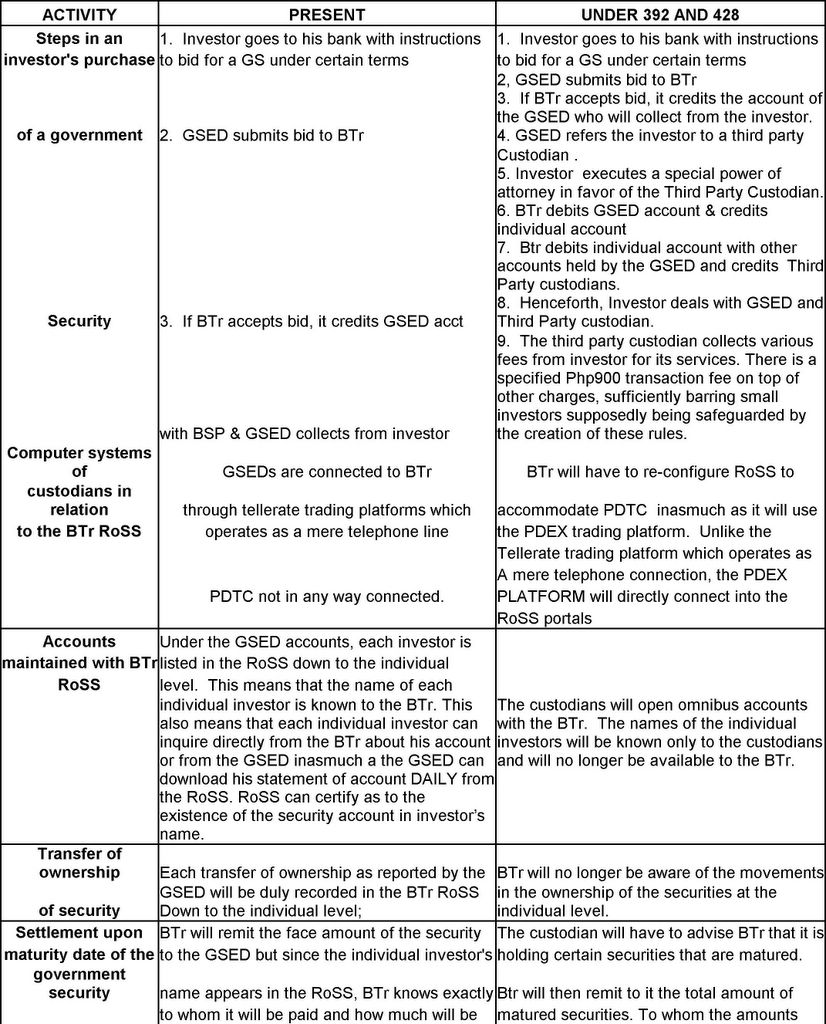

On the day she took her oath of office, she was instructed to implement these circulars even before she has had the time to study their merits. But prudence, however, dictated that she make an in depth study of the implications of the Circulars. And what did her study uncover? She learned that Circulars 392 and 428 were intended (1) to unduly favor a private entity, the Philippine Depository & Trust Corporation (PDTC) and (2) that their implementation would be grossly disadvantageous to the government and to the people.

The reasons for her conclusion follow:

Increase costs

1. Their implementation would increase the costs of investing in government securities that in turn would raise the country’s debt burden.

The very creation of the so-called third party custodians will cause the increase in the country’s debt burden. How?

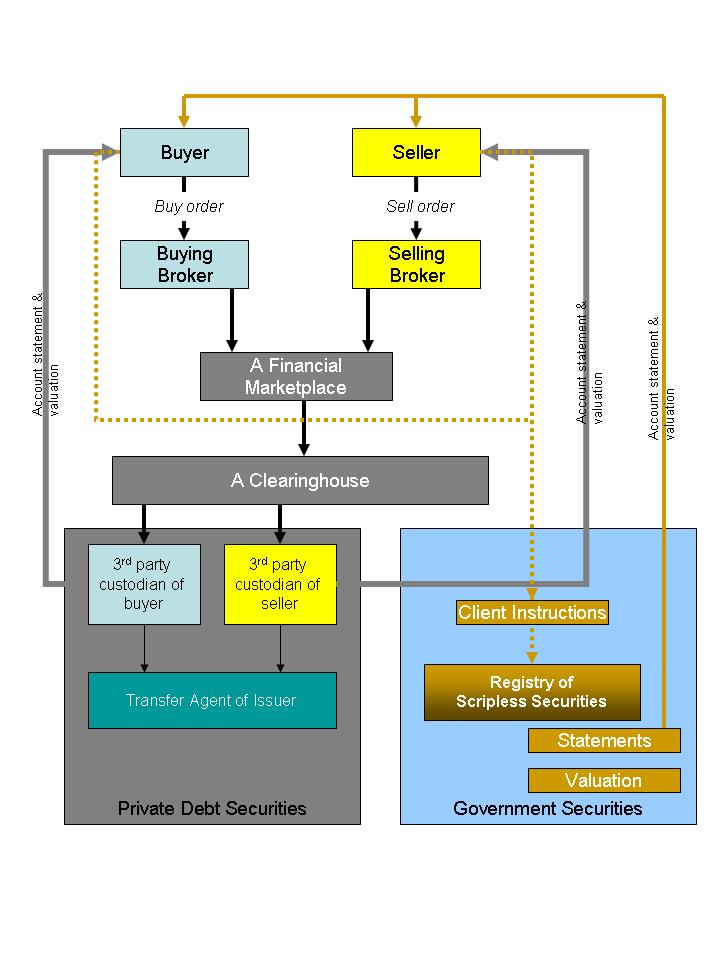

Selling of government securities is one of the means by which the government borrows domestically from the public. Right now the investors who buy government securities do so without having to pay any amount other than the cost of the government security. The buyer simply instructs his bank to submit a bid for a government security. Without much ado, the transaction is done and recorded in the RoSS in a matter of minutes.

If the investor has to course his purchase through a custodian, the custodian will charge him fees for its services.

Billions in additional costs

How much would such custodian fees amount to? According to Vicente Castillo, President and chief Executive Officer of PDS, a third party custodian, those fees would amount to half a billion pesos on an P800billion transaction.

P800 billion is a rather conservative estimate given that a government security is turned over several times, say twenty times, in a year. The cost could easily soar up P20 billion. Please note that the estimate was made by just one of six private custodians. To complete our discussion, we mention that the six are: four foreign banks, namely, Standard and Chartered Bank, Hongkong and Shanghai Bank, Deutch Bank and Citibank; one local bank, Bank of the Philippine Islands, and a non-bank, PDTC.

The country has some P2 trillion worth of government scripless securities in a given year. That is the magnitude of the transactions in scripless securities that normally pass through the RoSS annually. On the basis of the estimate, the costs of transactions in scripless securities - if private custodians were involved – would more or less be P20 billion.

If private custodians are allowed to lay their hands, as it were, on the scripless securities transactions, additional costs will have to be borne initially by the investor when he bids for the government security. The government, in turn, would have to increase the interest rate it pays on the scripless security to enable the investor to recover his added cost. In the end, the people would have to ultimately bear the added cost.

Foreign aided facility

2. The implementation of BSP Circulars 392 and 428 would also mean awarding a government infrastructure worth millions of pesos that the country has obtained from foreign aid and grants to a private entity without just compensation - - - for free! How will this be done?

For the PDTC (Philippine Depository and Trust Corporation) to function as third party custodian, it will have to connect its computer system to the computer system of the government operated by the Bureau of the Treasury. By making such a connection, PDTC will gain access to sensitive and vital debt data of the government and the sophisticated system that maintains such data. This system which is called the Registry of Scripless Securities or the RoSS was developed in 1996. RoSS has capabilities parallel to the advanced systems in the United States and Canada. There is nothing like it in Asia.

It looks, therefore, like only the PDTC will benefit from the implementation of the circulars in question. PDTC apparently wants to access, infiltrate and use the RoSS system of the Bureau of Treasury and for free!

It is said that the government wants to privatize the RoSS. If that is so, wouldn’t the proper way be to go through a public bidding? If RoSS is sold to private parties through public bidding, it will, no doubt, fetch a handsome sum equivalent to tens of billions of pesos given its superior quality and capacity. We have been at wit’s end on how to raise much needed revenues. Why give away such a valuable asset for free to a private company?

Imperils debt data

3. Implementation of 392 and 428 will endanger the integrity of the country’s debt data and the government’s ability to manage its debts. How?

The RoSS contains vital debt data which form the bases for the preparation of reports and the culling of statistics used by the government in crafting the budget and timing its borrowing efforts. It maintains detailed records down to the level of individual beneficial owners and is able to give the government fast information on who it owes money to, how much is owed and the terms of such obligations.

The third party custodians, as designed by 392 and 428 will maintain a general account of the investors buying the government securities, the details of which will be known only to them and no longer known by Bureau. It will create a ridiculous situation where in order to determine who the government owes any amount to and how much it owes, the Bureau would now have to ask six different entities, namely, Standard Chartered Bank, Hongkong Shanghai Bank, Citibank, Bank of the Philippine Islands and Deutch Bank and PDTC and, thereafter, do a reconciliation with each one. Coming up with reliable debt figures will be tedious, if not impossible.

Risky implementation

4. Implementation of 392 and 428 would be extremely risky for the government. Why?

PDTC is an accredited third party custodian by the Bangko Sentral. But it is capitalized at a mere P500M pesos. Given the trillions of pesos worth of securities it will handle, what protection can it offer the investors and the government for the scripless securities that will pass through its hands? While the comparison may be odious, let me say that, at least, a savings bank is capitalized for more - - at least P2.5 billion.

No sweat private gain

5. Implementation of 392 and 428 would mean the use of government funds for private gain.

Using government securities as a staple and connecting to the government’s computer, third party custodians will charge custodian and other fees. Meanwhile, it is the government which has to reconfigure the RoSS system to accommodate the custodians and continue to maintain and operate it so that the third party custodians can make a living! This is what the Tagalogs would call “sinisuerte talaga!”

Unnecessary circulars

6. Implementation 392 and 428 is unnecessary.

Implementing the circulars we are discussing gives no added value to the securities market or to the government. The circulars would only allow private custodian companies to intervene in a market that already functions efficiently with hardly a cost to the investor or the government. The market and the Bureau are being disrupted to accommodate and sustain the creations of Circulars 392 and 428. In fact, objections were raised by the Investment Houses Association of the Philippines, BAP Member Banks and Insurance companies. But like other well-meaning complaints, the objections all went unheeded.

Whenever the proponents of 392 and 428 are asked what advantage would there be in the creation of third party custodians, they answer that it will prevent a recurrence of a scam similar to the Bancap scam of 1994.

Bancap scam before RoSS

The answer is neither good nor honest. Everyone knows that the Bank of Commerce was involved in that scam in 1994. In fact, sad to say, its Treasurer, Rey Feliciano, later took his own life. The perpetrators of the scam, Ms. Marilyn Nite and her colleagues defrauded several banks, Planters Bank, among them, by selling a government security worth Php450 million several times resulting in multiple claimants over it.

When the Bancap scam occurred in 1994, the RoSS was not yet organized. At that time, government securities were evidenced by certificates. The lag time between the printing of the certificate of a government security and the sale of the security made possible multiple selling such that by the time the certificate was printed, more than two parties could claim ownership of the same security. At that time it was the Central Bank which was charged with the function of issuing government securities.

Since 1996, however, with the development of the RoSS, government securities have become paperless or what is now called “scripless”. These means that they begun to exist as electronic entries in the RoSS in 1966. Recording of transfers of ownership are done on “real time”, i.e., as soon as they transpire. This, as well as other standard features of the RoSS - delivery versus payment, report rendition to primary dealers, benchmarking, etc., will not allow a scam similar to that of Bancap to happen again.

Undisclosed facts

Now, private custodians would have a significant role to play only if government securities were still evidenced by certificates. In a paperless or scripless environment, what is there to take custody of?

Benchmarks, price transparency, price discovery, etc. – these are services that the RoSS is or is capable of rendering at no cost to the investor or to the government. In fact, investment rates are now available via short messaging system or text messages, and an investor can know the value of his or her securities practically anywhere in the world he or she might be a given moment.

These facts have not been disclosed to the public and to the authorities when Circulars 392 and 428 were issued.

Who benefits?

I wonder why the proponents are, as a newspaper has put in, “in such a murderous haste” to implement the circulars? Who are the powers behind these circulars? Who stands to benefit from them? If this so called “capital market reform” is so good why then was the country still downgraded by the credit raters in spite of the fact that Circulars 392 was issued on July 2, 2003 and circular 428 was issued in April, 2004?

Why had the Bangko Sentral refused to disclose to the Bureau the criteria with which they accredited the private custodians who would now take over the functions of the RoSS? Why is the BSP forcing the Bureau to simply allow the connection of the systems of the custodians with the RoSS without any asking any questions?

How odd that the very government agency – the Bureau of the Treasury - that is expected to implement the circulars and which is in a position to understand the consequences of their implementation has not been previously consulted. How can the issuance of mere bank circulars nullify existing laws that gave the Bureau of the Treasury its mandate? The Bangko Sentral cannot alter laws.

Why did the Department of Finance merely stand aside and allow an agency under it to be divested of its core function by the Bangko Sentral? Why this “short arms” deal? Did anyone in the Department of Finance and the Bangko Central benefit from this arrangement?

These questions need urgent answers.

Summing up

To sum up, implementing BSP Circulars Nos. 392 and 428 is wrong. It is harmful to the country and to the people. It should be stopped. The brains behind the idea of the circulars in question include BSP Governor Rafael Buenventura and the PDTC officials, Vicente Castillo, Cesar Crisol, Topper Coronel, Terry Montecillo, William Ferguson, Ms. Flor Tarriela and Roy Lacsamana. There’s a common thread that binds the lady and the gentlemen mentioned. They were all incorporators of PCD, the forerunner of the PDTC, and they were all former Citibankers about 15 to 20 years ago and worked in the Trust Division of the bank.

It is also interesting to note that the Articles of Incorporation of the Philippine Depository & Trust Corporation (formerly Philippine Central Depository, Inc) listed BSP governor Rafael Buenvaventura as a former member of its Board of Directors and one of its incorporators.

These are obviously powerful people who could cause the removal of honest and hardworking public servants who oppose their plans even if the latter acted out of a sincere belief that those plans would be disadvantageous to the government. It looks like the power they wield is practically limitless so that it needs to be checked.

It looks like the transfer of the Ross from the Bureau is being used to provide a golden parachute for some people to land a sinecure or even a lucrative position in the private sector once they retire from the public service. I hope I am wrong but the questions I have raised, I think, demand forthright and honest answers.

In fairness, the people who are named in this speech or who think that they are alluded to should be given the chance to respond before the proper Senate Committee which may be authorized to conduct an investigation relative to the questions raised in this speech.

Example Worthy of Emulation

In closing, let me say that the example set by Ms Norma Lasala in standing up against the wishes of her superiors for what she, after serious study, believe would be bad for the country, deservesemulation -- not condemnation, by other public servants. The insensitive manner by which she was removed as head of the Bureau of Treasury speaks volumes of the way this government is being run hellish to the honest and faithful public servant but heavenly to the corrupt and wayward public officials

{kind=link}

{kind=link}

{kind=link}

{kind=link}